Mobile App Development for Financial Services: Security, Compliance, and UX That Converts

We are no longer building apps that simply display account balances. In 2026, the most competitive financial services mobile applications are autonomous, intelligent, and deeply personalized capable of making real-time decisions on behalf of users without a single tap. The fintech market, valued at USD 394.88 in 2025 and race toward USD 1,760.18 Billion by 2034 at a CAGR of 18.20%.

The bar has never been higher and neither have the risks.

A single data breach in the financial sector now costs an average of $6.08 million per incident, a figure that is 22% above the global cross-industry average. At the same time, 89% of users say they would switch financial providers for a better app experience. That’s the paradox every fintech product team lives inside: harden the walls without locking out the user.

This blog breaks down what it truly takes to build a financial services mobile application in 2026 one that regulators approve, security teams respect, and users genuinely love.

The 2026 Fintech Landscape: What Has Fundamentally Changed

The transition happening in 2026 is not incremental it is architectural. Financial software has moved beyond digitizing paper processes into what industry analysts now call “agentic and autonomous financial systems.” AI agents are initiating transactions, flagging anomalies, adjusting investment allocations, and resolving support tickets without human intervention.

Simultaneously, regulatory frameworks have matured and multiplied. The EU’s DORA (Digital Operational Resilience Act) is now fully enforced, raising the bar for operational resilience and third-party risk management across all financial entities operating in Europe. In parallel, regulators globally are intensifying oversight on AI-driven financial decisions, demanding explainability, audit trails, and bias testing built directly into product architecture.

Security: The Architecture-First Imperative

Build Security In, Not On

The single most consequential decision in fintech mobile app development is treating security as an architectural constraint from day one not a feature layer bolted on pre-launch. Research confirms that building security into app architecture from the outset reduces vulnerabilities by up to 70% compared to retrofitting security measures after development.

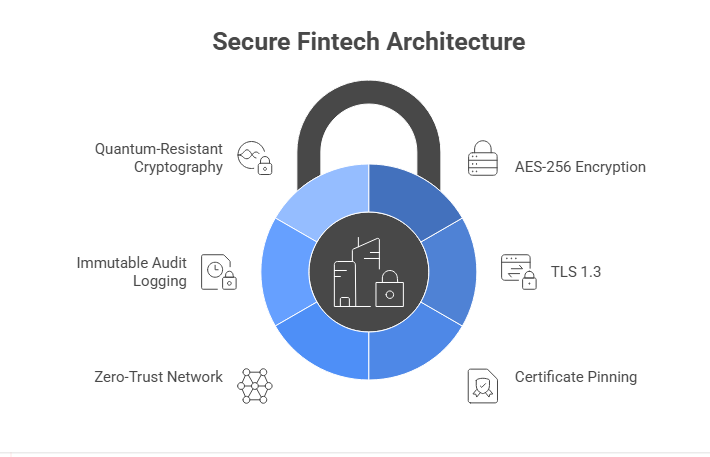

In 2026, a secure fintech app architecture must natively support:

- AES-256 encryption for data at rest, TLS 1.3 for all data in transit

- Certificate pinning to block man-in-the-middle attacks

- Zero-trust network architecture no implicit trust, even between internal services

- Tamper-evident, immutable audit logging with cloud-native solutions (AWS CloudTrail with S3 Object Lock or equivalent)

- Quantum-resistant cryptography no longer a future concern; financial institutions with long data retention obligations are actively piloting NIST-approved post-quantum standards now

Continuous Behavioral Authentication: Beyond Biometrics

In 2026, the security conversation has moved well past biometric login screens. The emerging standard is Continuous Behavioral Authentication (CBA) passive, always-on verification that analyzes how a user physically interacts with their device: typing cadence, swipe pressure, how they hold the phone, and scroll patterns. If the behavioral score remains high, the app stays unlocked and allows transactions without repeated re-authentication.

This is security that is invisible to legitimate users and impenetrable to bad actors the ultimate convergence of UX and protection.

Agentic AI and New Threat Surfaces

As Agentic AI take on broader transaction authority in fintech apps, they also create novel attack vectors. Prompt injection attacks targeting AI-driven financial assistants, model poisoning, and adversarial inputs designed to manipulate automated credit or fraud decisions are all active concerns in 2026.

Responsible fintech teams are now implementing:

- AI decision logging with full auditability

- Human-in-the-loop escalation thresholds for high-value autonomous actions

- Adversarial testing pipelines alongside standard QA

In 2026, 64% of financial institutions reported cyberattacks in the previous 12 months. Your threat model must assume breach, not just attempt to prevent it.

Compliance: From Checkbox to Competitive Advantage

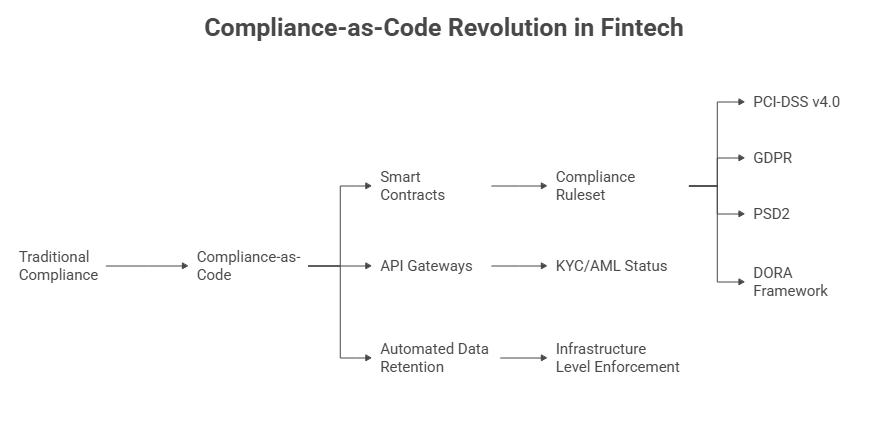

The Compliance-as-Code Revolution

The most significant shift in fintech compliance in 2026 is philosophical: leading development teams have stopped treating compliance as a legal sign-off step and started embedding it as code-level logic. Smart contracts that simply won’t execute if a transaction fails the compliance ruleset. API gateways that validate KYC/AML status in real time before any data exchange. Automated data retention and deletion policies enforced at the infrastructure level, not just documented in a policy PDF.

This is what regulators now call compliance-by-design and it is rapidly becoming the baseline expectation across PCI-DSS v4.0, GDPR, PSD2, and the EU’s DORA framework.

The 2026 Regulatory Landscape at a Glance

Regulation | Region | Key Focus in 2026 |

PCI-DSS v4.0 | Global | Customized implementation for emerging payment tech |

GDPR / DORA | EU/UK | Operational resilience + data rights enforcement |

CCPA / CPRA | California | Expanded consumer opt-out and data minimization rules |

KYC / AML | Global | AI-assisted real-time transaction monitoring |

DPDP Act | India | Expanding digital financial data protections |

Open Banking / PSD2 | EU | Mandatory API standardization |

Privacy by Design Is Not Optional

In 2026, privacy-conscious users actively evaluate apps before trusting them with their financial data. Regulators and users alike now expect:

- Minimal data collection aligned with the purpose of each feature

- Granular, understandable consent flows not walls of legal text

- Transparent explanations of how user data drives AI-powered recommendations

- One-sentence explainability for every AI-generated insight shown to a user

As one leading fintech UX principle puts it: “If a recommendation cannot be explained in one sentence to the user, it is not ready for the interface.”

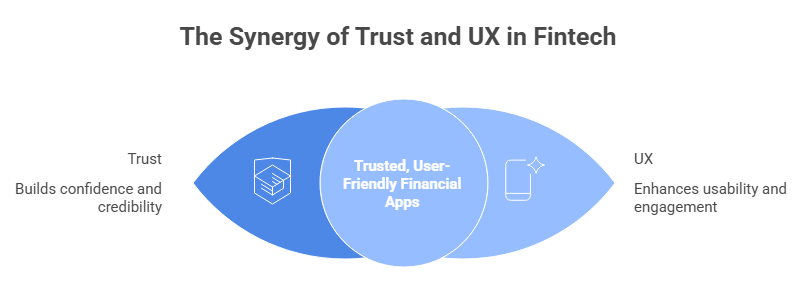

UX That Converts: Designing Financial Apps That Users Trust Daily

Trust Is Visual Before It Is Verbal

In financial services, every design decision communicates credibility or doubt before a user reads a single word. The visual language of your app spacing, color, typography weight, micro-copy, icon clarity either builds confidence or erodes it at a subconscious level. In 2026, leading fintech design systems are characterized by:

- Generous white space and strong visual hierarchy that reduce cognitive load

- Bold, high-contrast typography for key numbers (balances, rates, fees)

- Soft gradients, neutral palettes, and minimal borders as the prevailing aesthetic

- Transparent fee breakdowns and previews before the user commits to any action

Onboarding: The Highest-Stakes Interaction in Fintech

Onboarding is where most fintech apps win or lose their users permanently. Complex or lengthy onboarding remains the leading cause of user drop-off in financial apps. The 2026 standard for onboarding excellence includes:

- AI-powered eKYC with real-time document capture and OCR users verified in minutes, not days

- Biometric liveness detection to prevent spoofing and identity fraud during account creation

- Progressive disclosure each step collects only what’s needed at that exact moment

- Visual progress indicators showing users where they are and how long remains dramatically reduces abandonment

- Friction as a feature for high-value actions like large transfers, a deliberate biometric confirmation step makes users feel the weight and security of the action rather than anxious about it

AI-Driven Personalization: The Retention Engine

The highest-performing financial apps in 2026 use AI not just for fraud detection, but as the engine of daily engagement. Personalization in 2026 fintech goes well beyond spending categories:

- Predictive financial wellness nudges “You’re on track to hit your savings goal 12 days early”

- Behavioral segmentation replacing demographic segmentation for more relevant product recommendations

- User-controlled personalization toggles giving users visibility and choice over what data drives their experience

- Voice AI integration advanced voice interfaces now allow users to perform complex transactions, query balances, and manage budgets through natural conversation

The critical rule for 2026 personalization: transparency over creepiness. Users who feel their data is being used against them rather than for them disengage and they do not come back.

Final Thoughts

The financial apps winning in 2026 are not just the fastest or most feature-rich. They are the ones that have made security, compliance, and trust-first UX inseparable from the product itself where regulation is embedded in the codebase, where authentication is invisible to good actors, and where every design decision communicates confidence before a user reads a word.

If you are building or scaling a financial services mobile application and need a development partner who understands all of this from the ground up, App Maisters is built for exactly this challenge. As a specialized mobile app development company, App Maisters combines fintech regulatory knowledge, security-first architecture, and conversion-focused UX design to deliver financial applications that regulators approve, security teams trust, and users choose every day.

Ready to build a financial app that converts and keeps converting? Connect with App Maisters today.

FAQs

What security features are essential for a financial services mobile app?

AES-256 encryption, biometric authentication, MFA, and continuous behavioral authentication are the must-haves in 2026. App Maisters builds every fintech app with these security layers embedded from day one not added as an afterthought.

How do you ensure compliance in fintech mobile app development?

Compliance must be coded into the architecture from the start covering PCI-DSS, GDPR, KYC/AML, and regional regulations. App Maisters maps your full compliance requirements before a single line of code is written.

How much does it cost to develop a financial services mobile app?

Costs range from $20,000 for a basic app to $150,000+ for an enterprise-grade platform depending on features and compliance needs. App Maisters offers transparent, milestone-based pricing so there are zero surprises.

How long does it take to build a fintech mobile app?

A basic MVP takes 3–5 months, while a full-scale financial platform can take 9–18 months. App Maisters front-loads compliance and architecture planning to keep timelines on track from day one.

What is the best tech stack for fintech app development in 2026?

Flutter or React Native for cross-platform, Kotlin/Swift for native performance, and AWS or GCP for compliant cloud infrastructure are the leading choices. App Maisters recommends stacks based on your specific market, security needs, and scalability goals.

How does UX design affect conversions in a financial app?

89% of users would switch financial providers purely for a better app experience making UX a direct revenue driver. App Maisters uses a trust-first UX framework that turns first-time users into loyal, high-value customers.

Why choose App Maisters for financial services mobile app development?

App Maisters combines security-first engineering, regulatory expertise, and conversion-focused UX design under one roof. From MVP to enterprise scale, we build financial apps that regulators approve and users trust daily.